Datasets

US Equity

Create Subscriptions

Follow these steps to subscribe to a US Equity security:

- Create a

QuantBook. - Call the

add_equitymethod with a ticker and then save a reference to the US EquitySymbol.

qb = QuantBook()

spy = qb.add_equity("SPY").symbol tlt = qb.add_equity("TLT").symbol

To view the supported assets in the US Equities dataset, see the Data Explorer.

Get Historical Data

You need a subscription before you can request historical data for a security. On the time dimension, you can request an amount of historical data based on a trailing number of bars, a trailing period of time, or a defined period of time. On the security dimension, you can request historical data for a single US Equity, a subset of the US Equities you created subscriptions for in your notebook, or all of the US Equities in your notebook.

Trailing Number of Bars

To get historical data for a number of trailing bars, call the history method with the Symbol object(s) and an integer.

# DataFrame of trade and quote data single_history_df = qb.history(spy, 10) subset_history_df = qb.history([spy, tlt], 10) all_history_df = qb.history(qb.securities.keys(), 10) # DataFrame of trade data single_history_trade_bar_df = qb.history(TradeBar, spy, 10) subset_history_trade_bar_df = qb.history(TradeBar, [spy, tlt], 10) all_history_trade_bar_df = qb.history(TradeBar, qb.securities.keys(), 10) # DataFrame of quote data single_history_quote_bar_df = qb.history(QuoteBar, spy, 10) subset_history_quote_bar_df = qb.history(QuoteBar, [spy, tlt], 10) all_history_quote_bar_df = qb.history(QuoteBar, qb.securities.keys(), 10) # Slice objects all_history_slice = qb.history(10) # TradeBar objects single_history_trade_bars = qb.history[TradeBar](spy, 10) subset_history_trade_bars = qb.history[TradeBar]([spy, tlt], 10) all_history_trade_bars = qb.history[TradeBar](qb.securities.keys(), 10) # QuoteBar objects single_history_quote_bars = qb.history[QuoteBar](spy, 10) subset_history_quote_bars = qb.history[QuoteBar]([spy, tlt], 10) all_history_quote_bars = qb.history[QuoteBar](qb.securities.keys(), 10)

The preceding calls return the most recent bars, excluding periods of time when the exchange was closed.

Trailing Period of Time

To get historical data for a trailing period of time, call the history method with the Symbol object(s) and a timedelta.

# DataFrame of trade and quote data single_history_df = qb.history(spy, timedelta(days=3)) subset_history_df = qb.history([spy, tlt], timedelta(days=3)) all_history_df = qb.history(qb.securities.keys(), timedelta(days=3)) # DataFrame of trade data single_history_trade_bar_df = qb.history(TradeBar, spy, timedelta(days=3)) subset_history_trade_bar_df = qb.history(TradeBar, [spy, tlt], timedelta(days=3)) all_history_trade_bar_df = qb.history(TradeBar, qb.securities.keys(), timedelta(days=3)) # DataFrame of quote data single_history_quote_bar_df = qb.history(QuoteBar, spy, timedelta(days=3)) subset_history_quote_bar_df = qb.history(QuoteBar, [spy, tlt], timedelta(days=3)) all_history_quote_bar_df = qb.history(QuoteBar, qb.securities.keys(), timedelta(days=3)) # DataFrame of tick data single_history_tick_df = qb.history(spy, timedelta(days=3), Resolution.TICK) subset_history_tick_df = qb.history([spy, tlt], timedelta(days=3), Resolution.TICK) all_history_tick_df = qb.history(qb.securities.keys(), timedelta(days=3), Resolution.TICK) # Slice objects all_history_slice = qb.history(timedelta(days=3)) # TradeBar objects single_history_trade_bars = qb.history[TradeBar](spy, timedelta(days=3)) subset_history_trade_bars = qb.history[TradeBar]([spy, tlt], timedelta(days=3)) all_history_trade_bars = qb.history[TradeBar](qb.securities.keys(), timedelta(days=3)) # QuoteBar objects single_history_quote_bars = qb.history[QuoteBar](spy, timedelta(days=3), Resolution.MINUTE) subset_history_quote_bars = qb.history[QuoteBar]([spy, tlt], timedelta(days=3), Resolution.MINUTE) all_history_quote_bars = qb.history[QuoteBar](qb.securities.keys(), timedelta(days=3), Resolution.MINUTE) # Tick objects single_history_ticks = qb.history[Tick](spy, timedelta(days=3), Resolution.TICK) subset_history_ticks = qb.history[Tick]([spy, tlt], timedelta(days=3), Resolution.TICK) all_history_ticks = qb.history[Tick](qb.securities.keys(), timedelta(days=3), Resolution.TICK)

The preceding calls return the most recent bars or ticks, excluding periods of time when the exchange was closed.

Defined Period of Time

To get historical data for a specific period of time, call the history method with the Symbol object(s), a start datetime, and an end datetime. The start and end times you provide are based in the notebook time zone.

start_time = datetime(2021, 1, 1) end_time = datetime(2021, 2, 1) # DataFrame of trade and quote data single_history_df = qb.history(spy, start_time, end_time) subset_history_df = qb.history([spy, tlt], start_time, end_time) all_history_df = qb.history(qb.securities.keys(), start_time, end_time) # DataFrame of trade data single_history_trade_bar_df = qb.history(TradeBar, spy, start_time, end_time) subset_history_trade_bar_df = qb.history(TradeBar, [spy, tlt], start_time, end_time) all_history_trade_bar_df = qb.history(TradeBar, qb.securities.keys(), start_time, end_time) # DataFrame of quote data single_history_quote_bar_df = qb.history(QuoteBar, spy, start_time, end_time) subset_history_quote_bar_df = qb.history(QuoteBar, [spy, tlt], start_time, end_time) all_history_quote_bar_df = qb.history(QuoteBar, qb.securities.keys(), start_time, end_time) # DataFrame of tick data single_history_tick_df = qb.history(spy, start_time, end_time, Resolution.TICK) subset_history_tick_df = qb.history([spy, tlt], start_time, end_time, Resolution.TICK) all_history_tick_df = qb.history(qb.securities.keys(), start_time, end_time, Resolution.TICK) # TradeBar objects single_history_trade_bars = qb.history[TradeBar](spy, start_time, end_time) subset_history_trade_bars = qb.history[TradeBar]([spy, tlt], start_time, end_time) all_history_trade_bars = qb.history[TradeBar](qb.securities.keys(), start_time, end_time) # QuoteBar objects single_history_quote_bars = qb.history[QuoteBar](spy, start_time, end_time, Resolution.MINUTE) subset_history_quote_bars = qb.history[QuoteBar]([spy, tlt], start_time, end_time, Resolution.MINUTE) all_history_quote_bars = qb.history[QuoteBar](qb.securities.keys(), start_time, end_time, Resolution.MINUTE) # Tick objects single_history_ticks = qb.history[Tick](spy, start_time, end_time, Resolution.TICK) subset_history_ticks = qb.history[Tick]([spy, tlt], start_time, end_time, Resolution.TICK) all_history_ticks = qb.history[Tick](qb.securities.keys(), start_time, end_time, Resolution.TICK)

The preceding calls return the bars or ticks that have a timestamp within the defined period of time.

Data Normalization

The data normalization mode defines how historical data is adjusted for corporate actions. By default, LEAN adjusts US Equity data for splits and dividends to produce a smooth price curve, but the following data normalization modes are available:

If you use ADJUSTED, SPLIT_ADJUSTED, or TOTAL_RETURN, we use the entire split and dividend history to adjust historical prices.

This process ensures you get the same adjusted prices, regardless of the QuantBook time.

If you use SCALED_RAW, we use the split and dividend history before the QuantBook's EndDate to adjust historical prices.

To set the data normalization mode for a security, pass a data_normalization_mode argument to the add_equity method.

spy = qb.add_equity("SPY", data_normalization_mode=DataNormalizationMode.RAW).symbol

When you request historical data, the history method uses the data normalization of your security subscription. To get historical data with a different data normalization, pass a data_normalization_mode argument to the history method.

history = qb.history(qb.securities.keys(), qb.time-timedelta(days=10), qb.time, dataNormalizationMode=DataNormalizationMode.SPLIT_ADJUSTED)

Wrangle Data

You need some historical data to perform wrangling operations. The process to manipulate the historical data depends on its data type. To display pandas objects, run a cell in a notebook with the pandas object as the last line. To display other data formats, call the print method.

DataFrame Objects

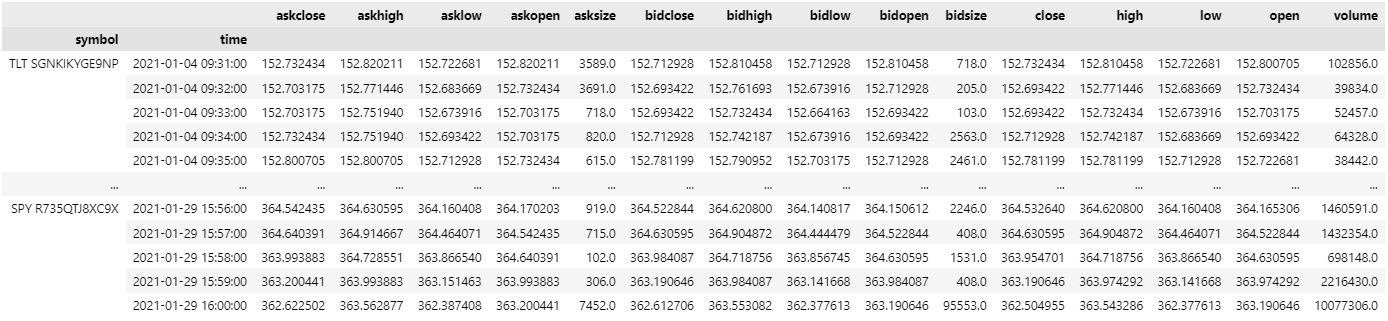

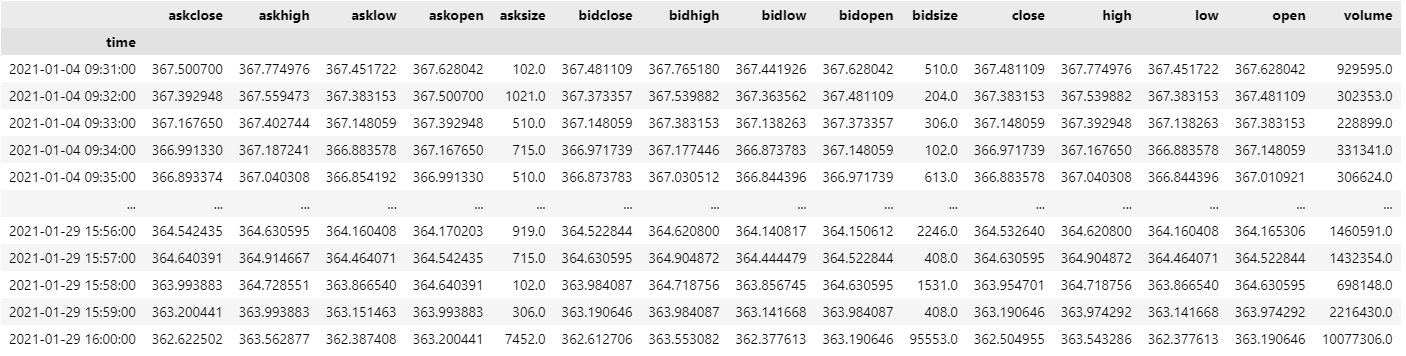

If the history method returns a DataFrame, the first level of the DataFrame index is the encoded Equity Symbol and the second level is the end_time of the data sample. The columns of the DataFrame are the data properties.

To select the historical data of a single Equity, index the loc property of the DataFrame with the Equity Symbol.

all_history_df.loc[spy] # or all_history_df.loc['SPY']

To select a column of the DataFrame, index it with the column name.

all_history_df.loc[spy]['close']

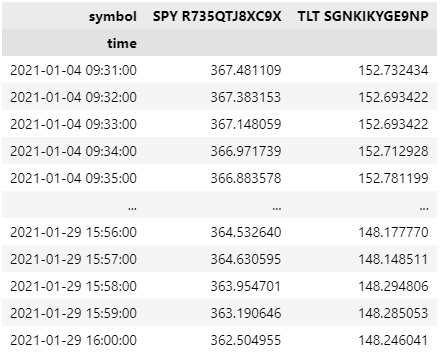

If you request historical data for multiple Equities, you can transform the DataFrame so that it's a time series of close values for all of the Equities. To transform the DataFrame, select the column you want to display for each Equity and then call the unstack method.

all_history_df['close'].unstack(level=0)

The DataFrame is transformed so that the column indices are the Symbol of each Equity and each row contains the close value.

If you prefer to display the ticker of each Symbol instead of the string representation of the SecurityIdentifier, follow these steps:

- Create a dictionary where the keys are the string representations of each

SecurityIdentifierand the values are the ticker. - Get the values of the symbol level of the

DataFrameindex and create a list of tickers. - Set the values of the symbol level of the

DataFrameindex to the list of tickers.

tickers_by_id = {str(x.id): x.value for x in qb.securities.keys}

tickers = set([tickers_by_id[x] for x in all_history_df.index.get_level_values('symbol')])

all_history_df.index.set_levels(tickers, 'symbol', inplace=True)

The new DataFrame is keyed by the ticker.

all_history_df.loc[spy.value] # or all_history_df.loc["SPY"]

After the index renaming, the unstacked DataFrame has the following format:

df["SPY close"]

Slice Objects

If the history method returns Slice objects, iterate through the Slice objects to get each one. The Slice objects may not have data for all of your Equity subscriptions. To avoid issues, check if the Slice contains data for your Equity before you index it with the Equity Symbol.

You can also iterate through each TradeBar and QuoteBar in the Slice.

for slice in all_history_slice: for kvp in slice.bars: symbol = kvp.key trade_bar = kvp.value for kvp in slice.quote_bars: symbol = kvp.key quote_bar = kvp.value

TradeBar Objects

If the history method returns TradeBar objects, iterate through the TradeBar objects to get each one.

for trade_bar in single_history_trade_bars: print(trade_bar)

If the history method returns TradeBars, iterate through the TradeBars to get the TradeBar of each Equity. The TradeBars may not have data for all of your Equity subscriptions. To avoid issues, check if the TradeBars object contains data for your security before you index it with the Equity Symbol.

for trade_bars in all_history_trade_bars: if trade_bars.contains_key(spy): trade_bar = trade_bars[spy]

You can also iterate through each of the TradeBars.

for trade_bars in all_history_trade_bars: for kvp in trade_bars: symbol = kvp.Key trade_bar = kvp.Value

QuoteBar Objects

If the history method returns QuoteBar objects, iterate through the QuoteBar objects to get each one.

for quote_bar in single_history_quote_bars: print(quote_bar)

If the history method returns QuoteBars, iterate through the QuoteBars to get the QuoteBar of each Equity. The QuoteBars may not have data for all of your Equity subscriptions. To avoid issues, check if the QuoteBars object contains data for your security before you index it with the Equity Symbol.

for quote_bars in all_history_quote_bars: if quote_bars.contains_key(spy): quote_bar = quote_bars[spy]

You can also iterate through each of the QuoteBars.

for quote_bars in all_history_quote_bars: for kvp in quote_bars: symbol = kvp.key quote_bar = kvp.value

Tick Objects

If the history method returns TICK objects, iterate through the TICK objects to get each one.

for tick in single_history_ticks: print(tick)

If the history method returns Ticks, iterate through the Ticks to get the TICK of each Equity. The Ticks may not have data for all of your Equity subscriptions. To avoid issues, check if the Ticks object contains data for your security before you index it with the Equity Symbol.

for ticks in all_history_ticks: if ticks.contains_key(spy): ticks = ticks[spy]

You can also iterate through each of the Ticks.

for ticks in all_history_ticks: for kvp in ticks: symbol = kvp.key tick = kvp.value

The Ticks objects only contain the last tick of each security for that particular timeslice

Plot Data

You need some historical Equity data to produce plots. You can use many of the supported plotting libraries to visualize data in various formats. For example, you can plot candlestick and line charts.

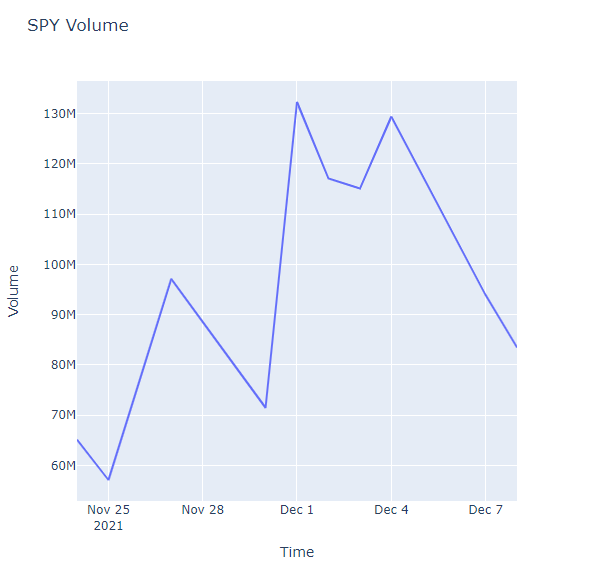

Candlestick Chart

Follow these steps to plot candlestick charts:

- Get some historical data.

- Import the

plotlylibrary. - Create a

Candlestickchart. - Create a

Layout. - Create the

Figure. - Show the plot.

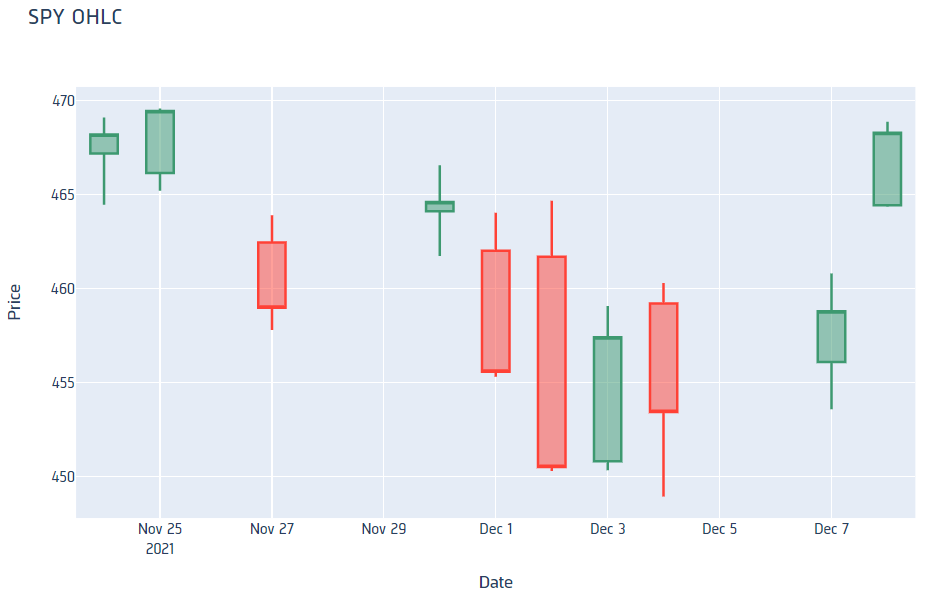

history = qb.history(spy, datetime(2021, 11, 23), datetime(2021, 12, 8), Resolution.DAILY).loc[spy]

import plotly.graph_objects as go

candlestick = go.Candlestick(x=history.index, open=history['open'], high=history['high'], low=history['low'], close=history['close'])

layout = go.Layout(title=go.layout.Title(text='SPY OHLC'), xaxis_title='Date', yaxis_title='Price', xaxis_rangeslider_visible=False)

fig = go.Figure(data=[candlestick], layout=layout)

fig.show()

Candlestick charts display the open, high, low, and close prices of the security.

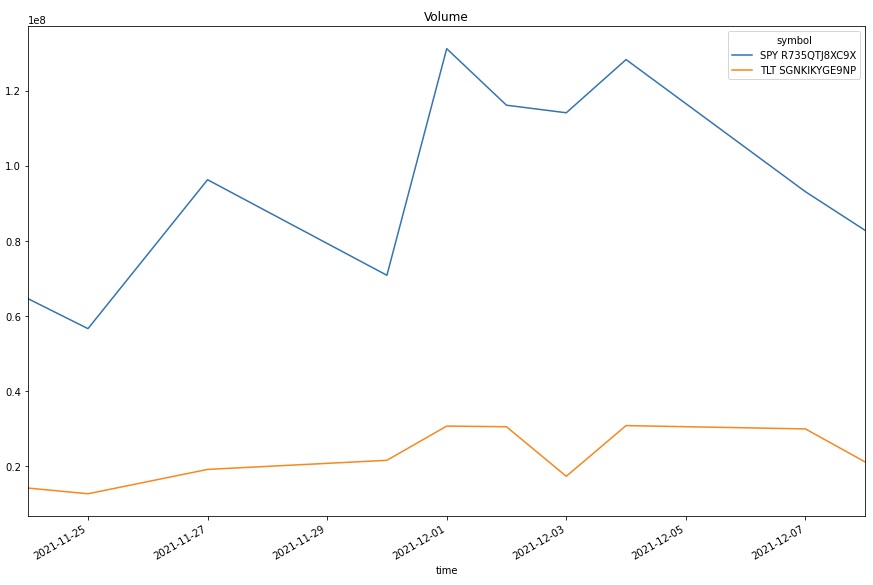

Line Chart

Follow these steps to plot line charts using built-in methods:

- Get some historical data.

- Select the data to plot.

- Call the

plotmethod on thepandasobject. - Show the plot.

history = qb.history([spy, tlt], datetime(2021, 11, 23), datetime(2021, 12, 8), Resolution.DAILY)

volume = history['volume'].unstack(level=0)

volume.plot(title="Volume", figsize=(15, 10))

plt.show()

Line charts display the value of the property you selected in a time series.

Common Errors

Some factor files have INF split values, which indicate that the stock has so many splits that prices can't be calculated with correct numerical precision. To allow history requests with these symbols, we need to move the starting date forward when reading the data or use raw data normalization. If there are numerical precision errors in the factor files for a security in your history request, LEAN throws the following error:

Examples

The following examples demonstrate some common practices for applying the US Equity dataset.

Example 1: 5-Minute Candlestick Plot

The following example studies the candlestick pattern of the SPY. To study the short term pattern, we consolidate the data into 5 minute bars and plot the 5-minute candlestick plot.

# Import plotly library for plotting. import plotly.graph_objects as go # Create a QuantBook qb = QuantBook() # Request SPY's historical data. spy = qb.add_equity("SPY") history = qb.history(spy.symbol, start=qb.time - timedelta(days=182), end=qb.time, resolution=Resolution.MINUTE) # Drop level 0 index (Symbol index) from the DataFrame history = history.droplevel([0]) # Select the required columns to obtain the 5-minute OHLC data. history = history[["open", "high", "low", "close"]].resample("5T").agg({ "open": "first", "high": "max", "low": "min", "close": "last" }) # Crete the Candlestick chart using the 5-minute windows. candlestick = go.Candlestick(x=history.index, open=history['open'], high=history['high'], low=history['low'], close=history['close']) # Create a Layout as the plot settings. layout = go.Layout(title=go.layout.Title(text=f'{spy.symbol} OHLC'), xaxis_title='Date', yaxis_title='Price', xaxis_rangeslider_visible=False) # Create the Figure. fig = go.Figure(data=[candlestick], layout=layout) # Display the plot. fig.show()

You can also see our Videos. You can also get in touch with us via Discord.

Did you find this page helpful?