Introduction

A Hidden Markov Model (HMM) estimates the probability an asset will continue similar behavior or jump to another state, making it a great tool to predict the current market regime (trending up, ranging, or trending down). In this micro-study, we implement a 3-component HMM strategy to detect market regimes and generate timely buy signals for liquid stocks on an intraday basis.

Background

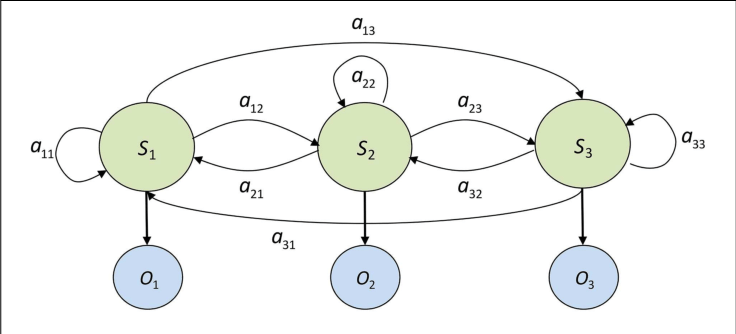

A HMM is a probabilistic model representing a sequence of events or observations, where the underlying process that generates the observations is not directly observable.

The use of HMMs in financial market analysis has gained traction in recent years. HMMs are powerful statistical models that can effectively capture the underlying, unobservable market states or "regimes" that drive asset price movements.

Their only input is price, so we wanted to focus on intraday timeframes to reduce the impact of the economy, politics and other macro factors. To start we chose 5-minute close price returns of the top 10 market cap stocks. These stocks tend to be highly liquid and less volatile, making them suitable for a rapid, intraday trading strategy. The 5-minute bar timeframe was sufficient to identify market regime shifts while maintaining a rapid response to intraday market fluctuations.

Implementation

To implement this on QuantConnect, we used universe selection, a data consolidator, and a returns indicator.

1. First, the strategy selects the top 10 US stocks by market capitalization. This is a fairly stable list as the top-10 don't change very frequently. By default this subscribes at minute resolution and updates daily.

def initialize(self):self.add_universe(lambda fundamental: [f.symbol for f in sorted(fundamental, key=lambda x: x.market_cap, reverse=True)[:10]])

2. We create a HMM object for the assets added to the algorithm, and set the random seed state to ensure the backtest result is repeatable. To remember the training state of the model we've created a model_month flag.

def on_securities_changed(self, changes):for added in changes.added_securities:added.model = hmm.GaussianHMM(n_components=3, n_iter=100, random_state=100)added.model_month = -1

3. Then we consolidate the minute data, and pipe the 5-minute bars into the on_consolidated event handler. We also create the rate-of-change indicator which will record the history of returns for our model.

added.roc = RateOfChange(1)added.roc.window.size = 150added.consolidator = TradeBarConsolidator(timedelta(minutes=5))added.consolidator.data_consolidated += self.on_consolidatedself.subscription_manager.add_consolidator(added.symbol, added.consolidator)

4. Later, when five minute bars are produced, we update the RateOfChange indicator. This automatically adds new return values to its rolling window, building the training data for our model. When we have enough data, the model is trained on the points available.

def on_consolidated(self, _, bar):security = self.securities[bar.symbol]security.roc.update(bar.end_time, bar.price)if security.roc.window.is_ready:if security.model_month != bar.end_time.month:security.model.fit(np.array([point.value for point in security.roc.window])[::-1].reshape(-1, 1))security.model_month = bar.end_time.month

5. The model can then use the latest 5-minute return to predict the current market regime for each asset. If P(positive) > P(negative), buy the stock, else short sell it. We use a fixed weight of 10% to ensure equal exposure.

post_prob = security.model.predict_proba(np.array([security.roc.current.value]).reshape(1, -1)).flatten()self.set_holdings(bar.symbol, 0.1 if post_prob[2] > post_prob [0] else -0.1)

Results

The implementation of a three-component Hidden Markov Model strategy for the top 10 market capitalization stocks yielded exceptional performance, with a Sharpe Ratio of 1.9. The model could quickly identify market regimes and capitalize on shifts in market conditions. By using a universe of liquid stocks we could efficiently trade intraday, and place multiple concurrent bets to smooth the overall return.

The algorithm parameter values (5, 150) were chosen at random. The strategy was resilient to a wide range of different parameters with all tests falling between 1.1-1.9 Sharpe Ratio.

As with any investment strategy, ongoing monitoring, optimization, and risk management practices are essential to maintain robust performance over time.

Lee Ashley

Very nice

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Remus Miclea

Thank for this, Louis, it got me started on the ML path, and look forward to learning more about it!

About the results: I cloned the code and checked the “baseline” results, given that the market was mostly in an uptrend, for the period considered (2023-Jan-01 till 2024-Sep-01, to be precise), and simply buying and holding could have been a successful strategy. To my surprise, I got better results, both as absolute return, as well as Sharpe ratio, when I forced the insights to be always UP (i.e. ignored any output of the HMM).

In other words, just buy-and-hold top 10 stocks, by market cap, outperforms the HMM model, for the said period. So, then, what is its value?

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Piyush Ravi

Hey!I was wondering why did you choose “n_components=3”. I tried your code with with

“n_components = 2” and

“direction = InsightDirection.UP if post_prob[-1] > post_prob [0] else InsightDirection.DOWN”.

It was giving slightly better results.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Ross Bernstein

Could this be tested on a basket of futures?

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Brandon Goyette

That would be interesting or maybe a basket of sector ETFs, across equities and maybe some with other less correlated exposures like a bitcoin ETF etc.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Kal Seehra

I played around with the asset selection a but and noticed that even in down markets, this HMM does not like to go short (typical short expose is less than 10%, even in a down market). Do you know why that would be? Is there a parameter that is biasing towards long exposure?

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Starteleport

Hi,

Thanks for the great article!

I've got a question on how exactly the mapping between hidden state index and a market regime is established?

I am referring to the following line:

Here, how do we arrive that we need to compare probability of the state #2 to the probability of the state #0? Could the meaning of these indexes/states suddenly change as we re-fit the model as the time goes? Does the meaning of indexes/states change with the change of the random_state parameter?

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Louis Szeto

Hi Starteleport

That was indeed a good question! Now, the state with the highest prevalence is at the lowest index by this library, but we can optimize the code by adding an identifier for which state is volatile and which is stable. You may just ask the model to predict the states of the data points it was used to train and check which state is more volatile to decide.

Best

Louis

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Petter Hansson

Here's the algo I'm broadcasting adapted from QT (link/attribution in code). I noticed it's trying to issue some too large orders at some points I don't really care to spend time figuring out why, and the code could use a cleanup. Also, if someone wanted to use this, carefully investigating slippage (particularly ensuring TLT and XIV have different values) is a necessity and possibly optimizing the order execution.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Petter Hansson

(Also, a disclaimer, with XIV it's good to familiarize with the the fact you could lose 100% of your investment overnight in some extreme circumstance... you're making money taking on tail risk.)

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Thomas Chang

@Petter,

>>you could lose 100% of your investment overnight in some extreme circumstance...

Yes. But I think maybe this is a little bit exaggerated? :-)

As Alex said: But you can easily re-construct (using pandas or even Excel) VXX and XIV back to 1990 by using their underlying indices...

If it's really could be re-constructed, one knows how to do the risk-management in his algo, right? And I think this is at least much 'saver' than doing PUT or SHORT.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Petter Hansson

Sure, just pointing out so nobody puts 100% of their capital into something like this. :-)

As for assuming the future will be same as the past, I don't recommend it in this case. Shorting volatility is a lot more popular now than in the past, which may lead to bigger kickbacks.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Petter Hansson

Good reading from time on time regarding the subject of risks in volatility, if somewhat gloomy.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Stevehank

Has anyone adapted any of the QT algorithms in below and successfully backtested in QC?

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Petter Hansson

I messed around with a ML version of something similar on QT but concluded the 'amazing' results in backtests were classical overfitting or out of date market inefficiencies. My ML version wanted to be long XIV mostly (go figure). These guys seem to arrive at something similar with better analysis than mine. That's not to say there isn't some signal in that data, but a few decision tree like rules or some linear classifier/regressor isn't going to cut it.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Stevehank

Much of the gains from strategies in the previous link are via UVXY, has anyone implemented a volatility strategy in QC with UVXY?

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Thomas Chang

With UVXY? You will short it or long it?

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Petter Hansson

Caveat: Shorting UVXY is easy in the same way that being long XIV is "easy" - algos that do either on average will likely work for some time for that reason.

Also, the backtest will not take into account short interest paid and by default IB's leverage limitation (IIRC now effectively cancelling out leverage you get versus XIV) isn't represented.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Stephen Oehler

Be careful about shorting something this volatile. I mentioned this in another post, but: you can not only lose your shirt but also your house by shorting something that has the potential to climb instantly for no reason. XIV has some protections in place to prevent it from climbing too rapidly (if one decides to thumb through the prospectus) but who knows the circumstances in which that would happen.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

TurboDZyl

I would like to implement a similar strategy as Alex did above, but selling call spreads or buying put options on UVXY, to limit risk. However if I simply add

option = self.AddOption("UVXY")in Initialize to be able to trade options, I get the following error once the backtest hits March 20, 2012:

Runtime Error: Microsoft.CSharp.RuntimeBinder.RuntimeBinderException: The best overloaded method match for `System.Collections.Generic.KeyValuePair<QuantConnect.Symbol,QuantConnect.Data.BaseData>.KeyValuePair(QuantConnect.Symbol, QuantConnect.Data.BaseData)' has some invalid arguments

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Jared Broad

turboDZyl -- Please avoid necro-posting or thread hijacking. If you have an issue with your specific algorithm post a new discussion and attach the backtest. To reference the original thread post a link to it in your new discussion.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Anthony FJ Garner

Given Quantopian's abandonment of personal automated trading I'm not surprised the refugees come over here. Especially since Python is now possible. What I would really need to trade VIX algorithmically is an automatically generated front month concatenated futures contract also showing spot VIX so as to be able to compute my favoured measure of contango/backwardation.

Although presumably one could just keep taking in the individual front month contract.

The big worry on XIV of course is a termination event. While VXX may seem unlikley to terminate (although I have not checked the prospectus) it is designed to go bust anyway and will just have another price consolidation (reverse split). I guess the bigger worry however is that the managers may not be unable to purchase futures contracts (to rebalance) during a spike in vol since the vast short brigade will be competing to gain cover and reverse their shorts.

Nonetheless a safer route to long XIV may just be deep ITM VXX puts.

I much look forward to working on Quantconnect now it has integrated Python.

I must say that my VIX adventure so far is a simple monthly rebalance between an inverse VIX fund such as XIV and a geared bond fund based on simple inverse volatility. Maximum drawdown on back testing is vastly reduced but of course the low correlation may not hold and XIV may suffer a liquidation event.

However, provided a liquidation event only occurs once in a blue moon, the method should enable one to survive. And you need to be ready with an alternative way to short VIX. Shorting VIX options seems hopeless. I can find little joy there although theoretically of course the options are based on futures. Nonetheless trading monthly VIX puts does not produce anywhere like the performance of a monthly short of the futures front month.

Perhaps I have made an error somewhere.

Anyway, I'm a Quantopian refugee although I have to say I had not been active there for about a year. I suggested they "offer bread today not jam tomorrow" and they seem to have heeded me as regards their competition. Nonetheless Quantopian is of little interest now that you can no longer trade using their framework. Especially since few have interest in the model they want to trade – a very low beta long short US equity approach.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Anthony FJ Garner

No, you can not go back to 1990 by using indices.

While the VIX index itself goes back as far as 1990, futures on the VIX only commenced in 2004 and options in 2006. Without futures there is no contango/backwardation and no XIV or VXX.

The S&P Index on which XIV is basd only goes back 10 years. What you need to do it to use the actual futures contracts to simulate XIV and VXX and you need to interpolate the front ans second month as per the index. The first chart below is the drawdown chart obtained by maintaining a 1x short position in the VIX front month futures contract since 2004. No interpolation applied. The second chart is the drawdown of the S&P 500 VIX Short Term Futures Inverse Daily Index TR since 2007. As you can see the drawdown for XIV in the last crash would have been close to 90%. Not pretty!

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Artemiusgreat

My implementation for C#.

The main problem that I see with Pairs Trading is that it's not clear when spread between correlated assets is enough to open positions. Prices of assets are often different and to compare them we need to normalize them, but usually after normalization we cannot compare actual prices because they are measured in abstract units, e.g. logarithms. Will it be enough to compensate commision if divergence is equal to 0.35 or 0.25? In my strategy I tried to use difference between fast and slow MAs, but it's also an approximation, and thus strategy has losses, because when MAs converge it doesn't mean that actual prices converged too.

Idea with RSI proposed by author also looks like an aproximation and also gives loses, maybe someone has a better idea for indicator that can display divergence between correlated assets?

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Alex Muci

@Anthony FJ Garner: you're right, I was imprecise - thanks for clarifying here.

Unfortunately, I've just learnt that European retail investors cannot puchase more XIV shares from 1st Jan 2018.

Long explanation: under the coming MIFID 2, the XIV is classified as a PRIIP ("Packaged Retails Investment and Insurance Product") and its issuer must publish a Key Information Document (KID) before private investors can make further purchases (we are, of course, allowed to keep or sell the shares we already own). The issuer of the XIV (Credit Suisse) apparently does not intend to publish a KID and this is the real issue.

I guess this is a good execuse (new regulations) for CS to constraint or limit some recent buying pressure on the ETN.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Anthony FJ Garner

Alex

How about SVXY? I usually register myself as a professional investor - I had better check I did so with IB. I wonder how that affects dealing in the derivatives. Not that there are any in XIVs case but of couse you could always buy VXX puts.

Regulators in general are not the brightes or most constructive of people.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Alex Muci

Anthony.

I don't know about SVXY. I've only received a communication from my pension provider regarding XIV (since in my portfolio), but nothing yet from IB. Perhaps you are right and regulations does not apply to me as professional. Worst case my solution is shorting VX futures - less granular and more risky (since being long XIV had at least the the beaty to have a bound loss, not a luxury you have with short futures).

Definetely something worth checking with IB.

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Anthony FJ Garner

Totally agree re shorting the futures - madness. If XIV becomes impossible (and also SVXY) I shall buy VXX puts. If those get banned well....um...its pointless using VIX options. Despite the fact they are linked to the relevant futures contract extracting the contango seems impossible from my back testing. I must triple check my back tester but....The returns using VIX options suck compared to using futures or the futures related ETFs.

Despite my scepticism I have also begun disaster insurance for my short VIX products using LEAPS going out two years, deep OTM. At least its some protection against a complete bust. Its a good strategy but it will be interesting to live throgh the coming shitstorm and survive....

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

To unlock posting to the community forums please complete at least 30% of Boot Camp.

You can continue your Boot Camp training progress from the terminal. We hope to see you in the community soon!