ORGANIZATIONS

ORGANIZATIONS

Contents

Research

Machine Learning Research

Introduction

Machine learning algorithms provide another way to analyze and conduct research on data. They allow us to detect patterns on large datasets and create predictive models. There are many machine learning libraries which make it easy to create, train and use various machine learning models. QuantConnect supports many of the popular frameworks like SciKit and TensorFlow. You can find a full list of the supported libraries in the Machine Learning documentation.

Using Scikit-Learn

Scikit-learn is a framework that provides us with many ready to use algorithms for classification and regression, like support vector machines (SVM), random forests, and many more. SciKit is great to use if you want to quicky test an idea or hypothesis using a machine learning algorithm, without having to worry about building a model from the ground up.

Linear Regression Example

Regression uses past data to train a model that can predict future data. There are many different regressions with various degrees of sophistication. Linear regression is one of the simple of these models. Linear regression aims to create a linear approximation of future data. Scikit provides the LinearRegression method which creates a ready to go regression model for us to train and use.

Let's create a linear regression model trained on 30 days of historical SPY price data and use to predict the next 30 days of data. We'll need to first import our dependencies from SciKit and subscribe to SPY data.

from sklearn.linear_model import LinearRegression

qb = QuantBook()

spy = qb.AddEquity("SPY")

Next, let's make a history call for the last 60 days of price data. We will use the first 30 days to train our model and then use the next 30 days to test our model.

# 60 days of SPY data spy_history = qb.History(spy.Symbol, 60, Resolution.Daily) # Drop the symbol index from multi-index dataframe spy_history = spy_history.reset_index(level=0, drop=True) # Get list of 60 days of open prices from dataframe prices = list(spy_history['open'])

The linear regression model requires two series, train_X and train_Y, to train our model with. We want to predict prices using our model so the prices will be our train_Y. We can use a time series starting at t=0 as our train_X.

# Create time series list of training range train_range = range(30) # Format time series data into form compatible with LinearRegression train_X = np.column_stack([np.ones(len(A)), A]) # First 30 days of price data used for training train_Y = price[:30] # Define LinearRegression model from scikit reg = LinearRegression() # Fit model with training data reg.fit(train_X, train_Y)

Now we can test the model's predictions on the next 30 days of data against the actual prices. First, we create a test_X for the entire 60 days of time, then feed the model with it and save its predictions.

# 60 day time series test_range = range(60) # Format time series data test_X = np.column_stack([np.ones(len(test_range)), test_range]) # Use linear regression model to predict prices prices_pred = reg.predict(test_X)

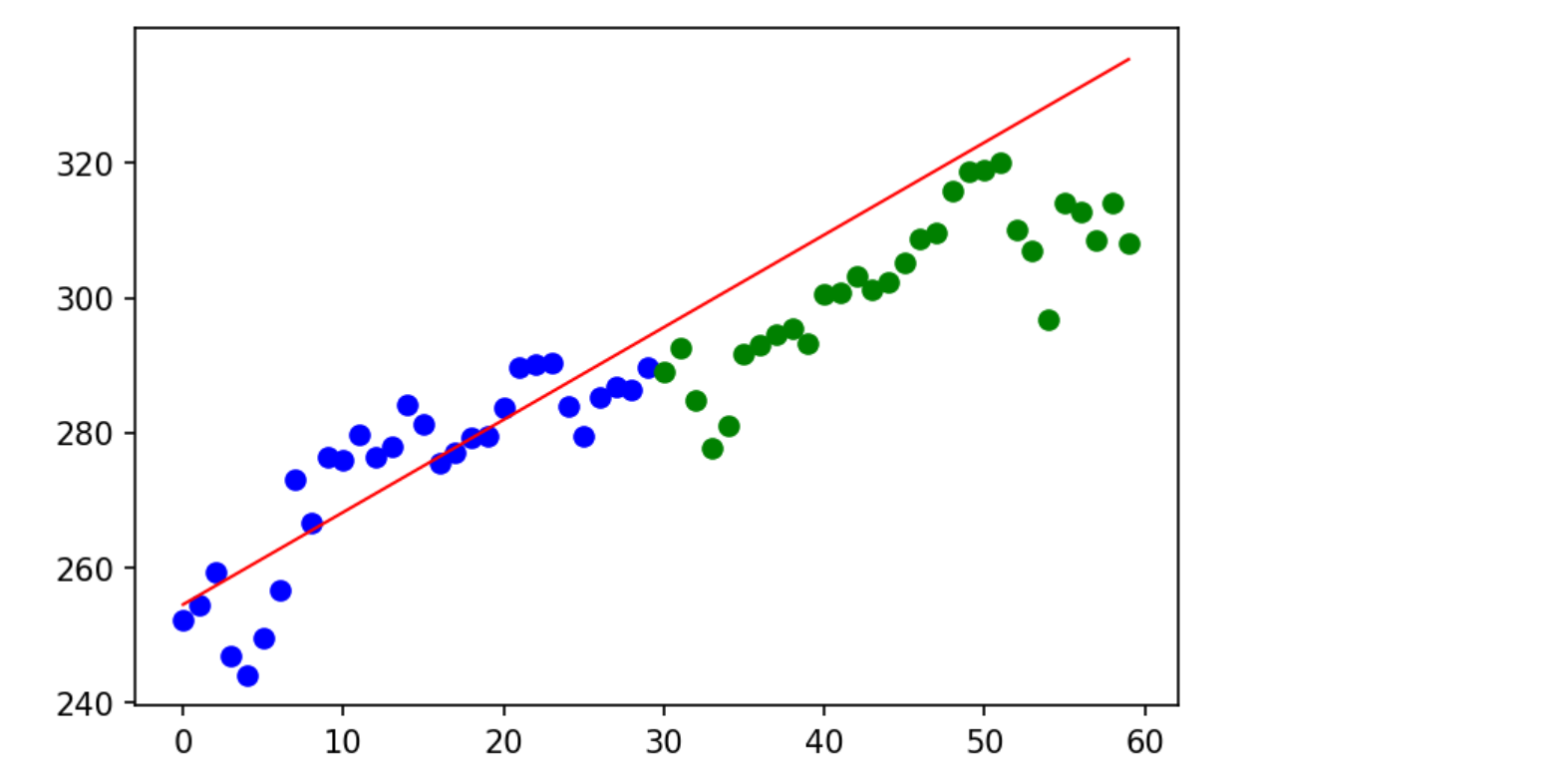

To visualize how well our model performs, we can plot the price data overlayed with the linear model. Let's split the price data scatter plot into two sections, blue for our training data and green for our testing data.

# The first 30 days of price data used to train model plt.scatter(test_range[:30], prices[:30], color='blue') # The next 30 days of price data plt.scatter(test_range[30:60], prices[30:60], color="green") # The linear regression model plt.plot(test_range, prices_pred, color='red', linewidth=1)

Using TensorFlow

TensorFlow is a low-level library that we can use to implement machine learning algorithms. Unlike scikit, TensorFlow does not have any ready to use algorithms, Instead, TensorFlow provides the building blocks to implement the algorithms we need. TensorFlow is especially great for implement deep learning algorithms and working with large datasets since it allows us to take advantage of GPU's for training our models.

Preparing Data For Training and Testing

Let's create a neural network that predicts future prices given past prices. We'll build our network with TensorFlow and then train it using historical data. We can then test our model by visualizing its predictions against actual historical prices. First, we'll need to retrieve historical data for SPY.

import tensorflow as tf

qb = QuantBook()

spy = qb.AddEquity("SPY").Symbol

# retrieve close data

data = qb.History(spy,

datetime(2020, 6, 22),

datetime(2020, 6, 27),

Resolution.Minute).loc[spy].close

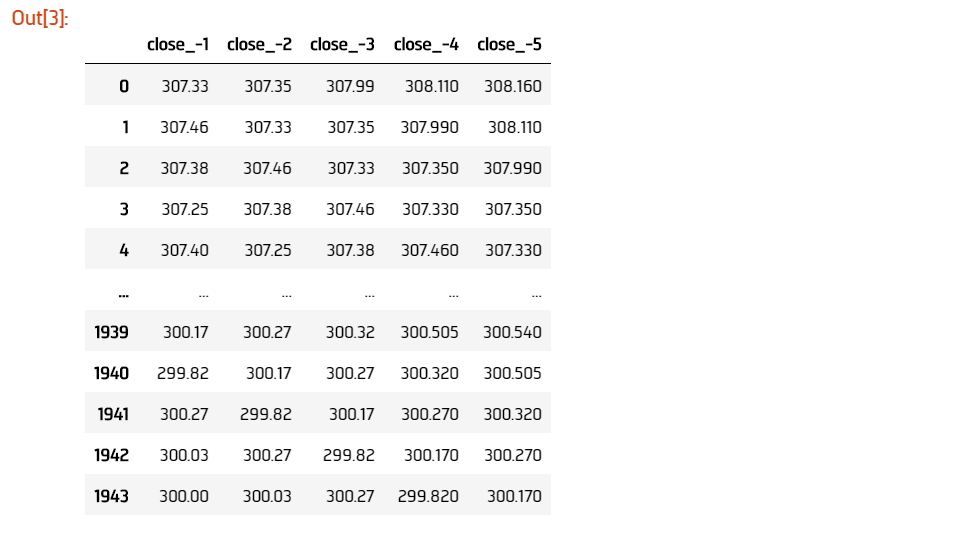

We'll feed our network the last 5 close prices to predict the next close. Let's format our data into our input dataframe X by offsetting our historical close prices.

# Feeding 5 input past prices to predict the next price

lookback = 5

# Series to hold each set of input prices

lookback_series = []

# Offsetting close data by length of lookback

for i in range(1, lookback + 1):

df = data.shift(i)[lookback:-1]

df.name = f"close_-{i}"

lookback_series.append(df)

# Formatting offset data into input format

X = pd.concat(lookback_series, axis=1).reset_index(drop=True)

Since we'd like to predict the closing price of SPY 1 timestep into the future, we should create a dataframe containing this data. This will serve as our neural network's training and testing output Y.

# Shift our time series close data by 1 Y = data.shift(-1)[lookback:-1].reset_index(drop=True)

We can then split our data into training and testing sets using scikit-learn's train_test_split. We will use the training set to train our model and then assess the network's predictions against the test data. Let's use a third of our data to test and the remaining to train our model.

# import scikit-learn's train_test_split method from sklearn.model_selection import train_test_split # split historical data into training and testing sets X_train, X_test, y_train, y_test = train_test_split(X, Y, test_size=0.33, shuffle=False)

Building Models

Let's build a neural network with 3 hidden layers and an output layer. We'll have 32 neurons in our first layer, 16 in our second, and 8 in our third layer.

# Initialize a tensorflow graph object tf.reset_default_graph() sess = tf.Session() # parameters for our neural network num_factors = X_test.shape[1] num_neurons_1 = 32 num_neurons_2 = 16 num_neurons_3 = 8 # Placeholders for our inputs and outputs X = tf.placeholder(dtype=tf.float32, shape=[None, num_factors], name='X') Y = tf.placeholder(dtype=tf.float32, shape=[None])

Next, we can build our model layer by layer. We will need a set of weights and biases for each layer.

# Initializers weight_initializer = tf.variance_scaling_initializer(mode="fan_avg", distribution="uniform", scale=1) bias_initializer = tf.zeros_initializer() # Hidden weights W_hidden_1 = tf.Variable(weight_initializer([num_factors, num_neurons_1])) bias_hidden_1 = tf.Variable(bias_initializer([num_neurons_1])) W_hidden_2 = tf.Variable(weight_initializer([num_neurons_1, num_neurons_2])) bias_hidden_2 = tf.Variable(bias_initializer([num_neurons_2])) W_hidden_3 = tf.Variable(weight_initializer([num_neurons_2, num_neurons_3])) bias_hidden_3 = tf.Variable(bias_initializer([num_neurons_3])) # Output weights W_out = tf.Variable(weight_initializer([num_neurons_3, 1])) bias_out = tf.Variable(bias_initializer([1])) # Hidden layer hidden_1 = tf.nn.relu(tf.add(tf.matmul(X, W_hidden_1), bias_hidden_1)) hidden_2 = tf.nn.relu(tf.add(tf.matmul(hidden_1, W_hidden_2), bias_hidden_2)) hidden_3 = tf.nn.relu(tf.add(tf.matmul(hidden_2, W_hidden_3), bias_hidden_3)) # Output layer output = tf.transpose(tf.add(tf.matmul(hidden_3, W_out), bias_out), name='outer')

Training Models

We will need a loss function and an optimizer function to train our model; we can use TensorFlow's built-in tf.squared_difference and tf.train.AdamOptimizer(), respectively. An epoch is an iteration of our entire training set. Let's train our model for 20 epochs.

# Define loss and optimizer functions

loss = tf.reduce_mean(tf.squared_difference(output, Y))

optimizer = tf.train.AdamOptimizer().minimize(loss)

sess.run(tf.global_variables_initializer())

# Define training parameters

batch_size = len(y_train) // 10

epochs = 20

# Train Model

for _ in range(epochs):

for i in range(0, len(y_train) // batch_size):

start = i * batch_size

batch_x = X_train[start:start + batch_size]

batch_y = y_train[start:start + batch_size]

sess.run(optimizer, feed_dict={X: batch_x, Y: batch_y}))

Testing Models

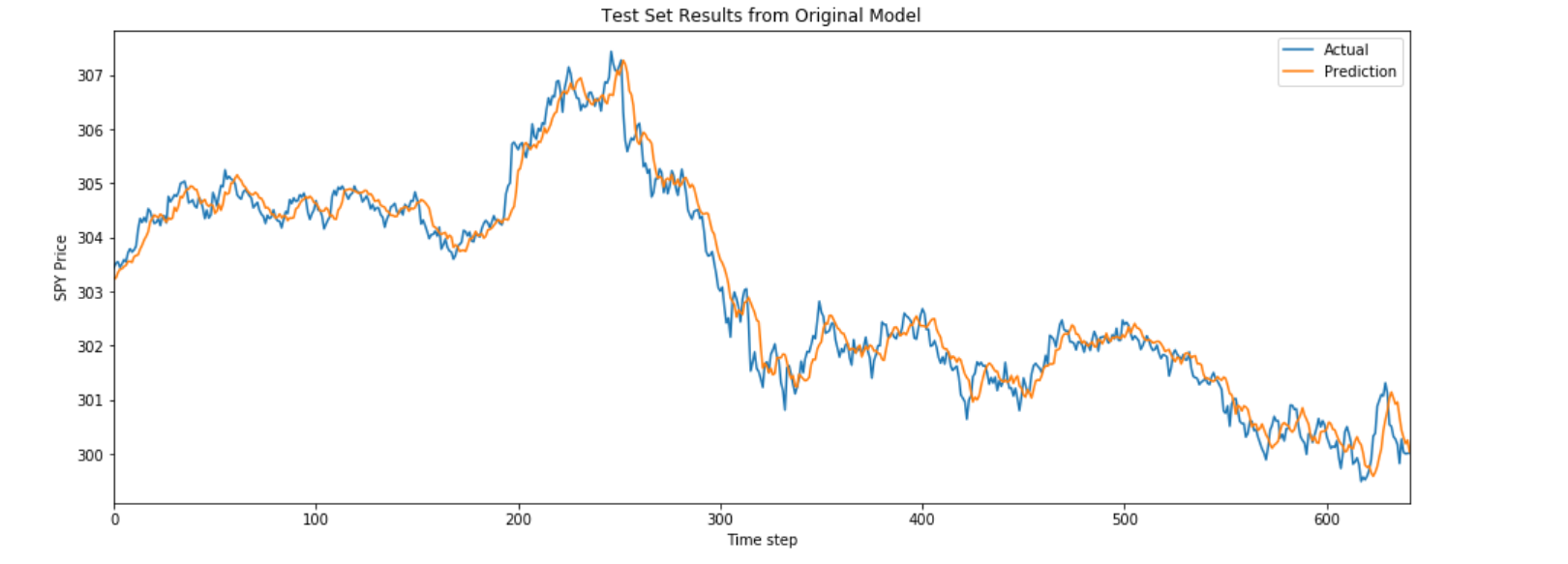

Finally, let's test how accurate our model is by plotting its predictions against actual price data.

prediction = sess.run(output, feed_dict={X: X_test})

prediction = prediction.reshape(prediction.shape[1], 1)

y_test.reset_index(drop=True).plot(figsize=(16, 6), label="Actual")

# Plot predictions

plt.plot(prediction, label="Prediction")

plt.title("Test Set Results from Original Model")

plt.xlabel("Time step")

plt.ylabel("SPY Price")

plt.legend()

plt.show()

Using Keras

Keras is a high level library for neural networks. Keras was designed to be modular fast and easy to use. It allows for easy and quick implementations of models.

Neural networks provide a way to predict future prices based on past prices. In order to accomplish this in Keras, we will need to create a Sequential model and train it with historical data. After our model has been trained, we can test its accuracy by comparing its predictions against historical prices. First, let's import the necessary dependencies and subscribe to SPY data.

from keras.models import Sequential

from keras.layers import Dense, Flatten

from keras.optimizers import RMSprop

spy = qb.AddEquity("SPY")

Preparing Data For Training and Testing

Let's create a model that predicts the next percent change in closing price given 5 days of OHLCV data. We can make a history call for 360 days of data that we will use to both train and test our model.

spy_hist = qb.History(qb.Securities.Keys, 360, Resolution.Daily).loc['SPY']

# n_tsteps is the number of time steps at and before time t we want to use

# to predict the close price at time t + 1

# in this case it is 5

n_tsteps = 5

# this helps normalizes the data

df = data.pct_change()[1:]

features = []

labels = []

# Format data into inputs/features and outputs/labels

for i in range(len(df)-n_tsteps):

input_data = df.iloc[i:i+n_tsteps].values

features.append(input_data)

label = df['close'].iloc[i+n_tsteps]

labels.append(label)

X, y = np.array(features), np.array(labels)

Now we can split our historical data into training and testing sets. We'll use the first 300 days of data to train our model and the remaining days to test our model.

# split data into training/testing sets X_train = X[:300] X_test = X[300:] y_train = y[:300] y_test = y[300:]

Building Models

Next, we create our neural network model. The Keras Sequential model allows us to create a neural network layer by layer. We will use a neural network with 2 hidden layers and a flatten layer, which is required because our input data is 2-dimensional; i.e. there are 5 input days, each with OHLCV data. We'll use a mean-square error loss function with an RMSprop optimizer function.

model = Sequential([

# 5 input variables (OHLCV) by 5 time steps

Dense(10, input_shape=(5,5), activation='relu'),

Dense(10, activation='relu'),

# Flatten layer required because input shape is 2D

Flatten(),

# since we are performing regression, we only need 1 output node

Dense(1)

])

# Set loss function and optimizer

model.compile(loss='mse',

optimizer=RMSprop(0.001),

metrics=['mae', 'mse'])

Training and Testing Models

Keras allows for easy training using the model.fit(x_train, y_train, epochs) method. This method iterates through our training set once for each epoch.

# Train model with training data model.fit(X_train, y_train, epochs=5)

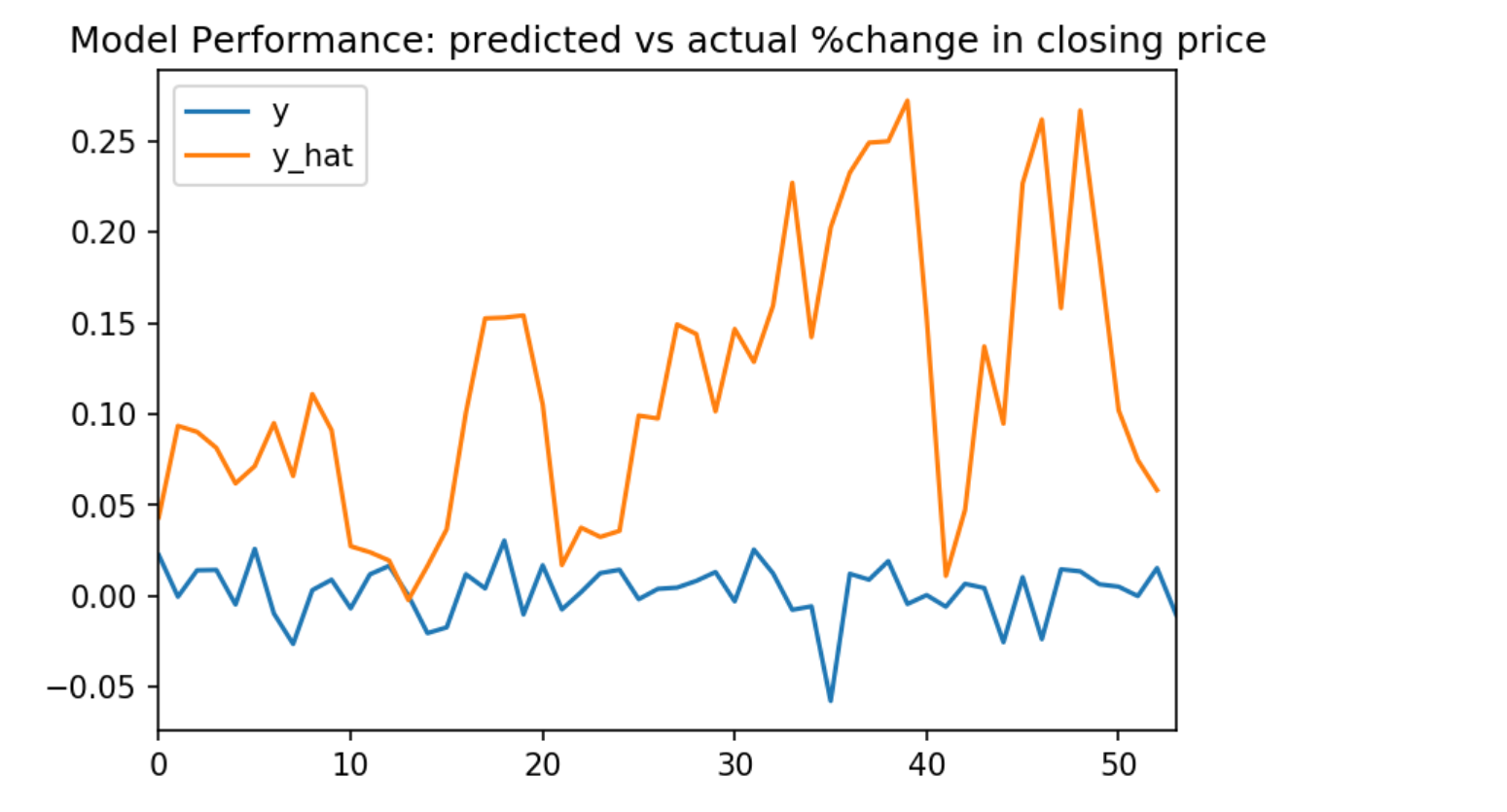

Finally, let's visualize our neural networks accuracy by plotting its predictions alongside the historical prices changes. We can use model.predict(x_test) to retrieve our model's predictions on the test set. Then we can format our predicted prices and actual historical changes in a dataframe, and plot that dataframe.

y_hat = model.predict(X_test)

df = pd.DataFrame({'y': y_test.flatten(), 'y_hat': y_hat.flatten()})

df.plot(title='Model Performance: predicted vs actual %change in closing price')

Resource Limitations

Training machine learning algorithms can be quite computationally expensive. There is a 10 minute limit on a time single loop in backtesting. This means that if we are training a model on a large dataset, algorithm may time out. The self.Train method increases this limit to 30 minutes, allowing us more time to train our model. You can learn more in the Machine Learning documentation.

Saving Models with the Object Store

The Object Store is a project specific storage space available in the QuantConnect web environment. We can use the Object Store to save trained models for future use. You can learn more about the Object Store in the Machine Learning documentation.

Keras

In order to save our model, we can first use serialize_keras_object from the keras.util library to convert our model into a json. Then we can convert our json into string using json.dumps. Finally, we save our model using qb.ObjectStore.Save. We will need to provide the Object Store a key to reference our saved object.

model_key = 'my_model' import json from keras.utils.generic_utils import serialize_keras_object modelStr = json.dumps(serialize_keras_object(model)) qb.ObjectStore.Save(model_key, modelStr)

Then we can load our model from the Object Store using qb.ObjectStore.Read with our key. We should make sure our key exists in the Object Store before attempting to access it. Then we can convert our string back into a json and finally create a sequential model from it using Sequential.from_config.

if qb.ObjectStore.ContainsKey(model_key):

modelStr = qb.ObjectStore.Read(model_key)

config = json.loads(modelStr)['config']

model = Sequential.from_config(config)

You can also see our Tutorials and Videos. You can also get in touch with us via Discord.

Did you find this page helpful?