Hey everybody,

so I copied a code from my colaboratory into quantconnect and changed the data source accordingly. This results in a return dataframe of stocks with their respective daily returns.

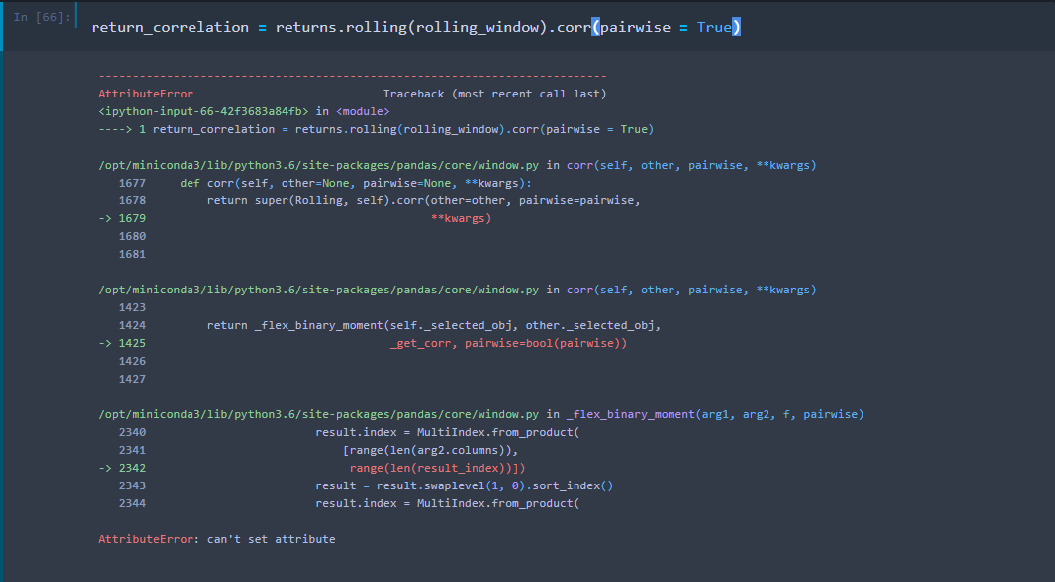

Fine so far. What I want to do is calculate the respective smoothed correlations between each pair. I did that previously through the code snippet below. This time however, I received an error, which I found no documentation on.

Could someone tell me what I am doing wrong here? Because it works in my colaboratory environment.

Best regards

Jared Broad

Can you please share a mock example so we can better assist?

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Korbinian Gabriel

Hey Jared,

thanks for your reply. Sure, here is the research book:

best regards

Derek Melchin

Hi Korbinian Gabriel,

Unfortunately, our research environment is currently using a version of numpy that does not support rolling pairwise correlation calculations. We have a scheduled update/addition of python packages coming and can get back to you after it is complete.

Best,

Derek

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Samuel Schoening

Hello Derek, I am also interested in rolling correlation calculations. Was just wondering if you had any updates on this now?

Derek Melchin

Hi Samuel,

Rolling correlations are now possible. See the attached notebook for an example.

Best,

Derek Melchin

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

Korbinian Gabriel

The material on this website is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory services by QuantConnect. In addition, the material offers no opinion with respect to the suitability of any security or specific investment. QuantConnect makes no guarantees as to the accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances. All investments involve risk, including loss of principal. You should consult with an investment professional before making any investment decisions.

To unlock posting to the community forums please complete at least 30% of Boot Camp.

You can continue your Boot Camp training progress from the terminal. We hope to see you in the community soon!